USDC, USDT, DAI, USDY, USDe?

SO MANY OPTIONS.

Back in April I wrote the first version of this article, after a livestream where I asked which stablecoins everyone is using and trusting. The questions that came back were really good, and the article ended up being one of my most bookmarked pieces.

Three months later the numbers moved, few new names showed up, and I could test the one I found more interesting for a while.

First, the honest picture of where the market is right now.

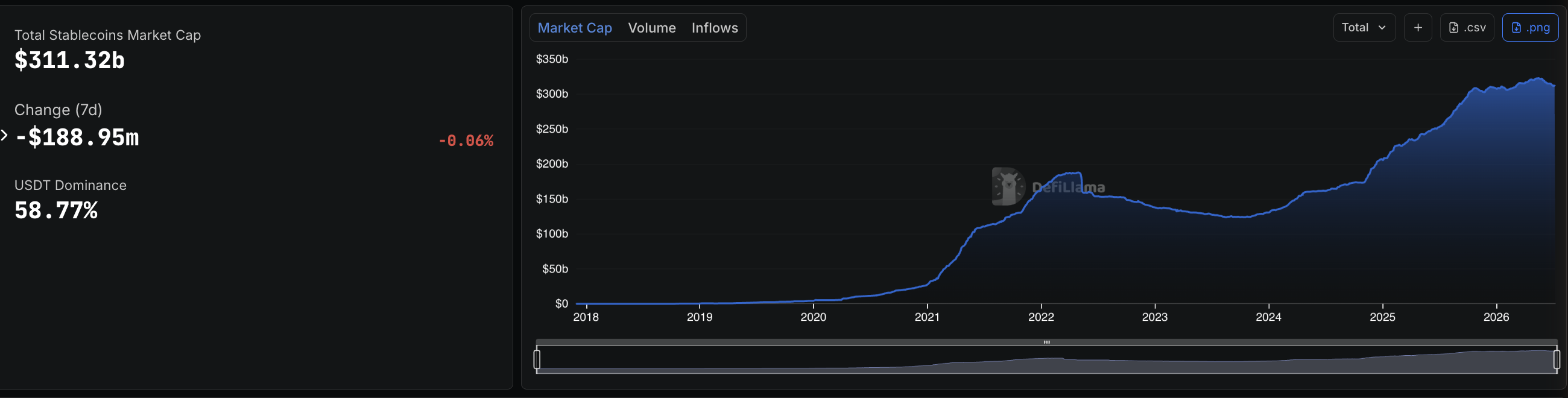

The whole stablecoin market sits above $310 billion as of July 2026, almost double what it was two years ago. USDT (Tether) is still the giant, around $183 billion and roughly 59% of the entire market. USDC (Circle) is second at about $73 billion. Between the two of them, more than 80% of all stablecoins in existence.

Source: DefiLlama, stablecoin market overview, July 8 2026

What Is Actually Happening Once You Hold USDT or USDC

Here is the part just the 1% of the top 1% will actually ask.

If I'm "parking" my dollars with Circle or Tether, those companies are taking my money, putting it in US Treasuries, and earning yield on it, just like any Treasury holder. In a year this is Billions in profit, yes, the B word not Millions.

As a supporter, a very small fish holder, what are we getting back from it?

Nothing. Zero. My USDC sits at $1 forever.

Isn't this exactly the thing we said we hated about banks?

Actual footage of me once I got it.

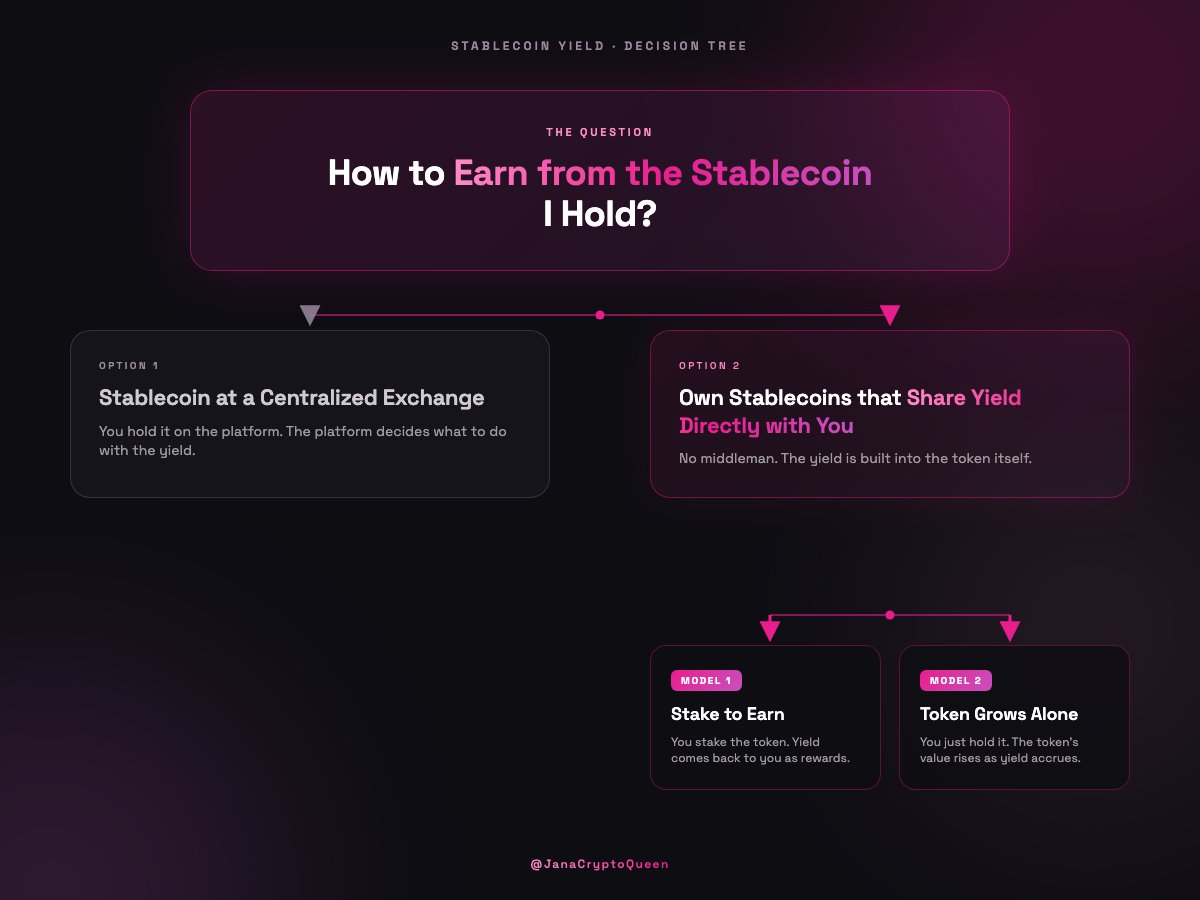

Which Option Do We Have?

Option 1: Park your stables on a centralised exchange

If your money is already sitting on Binance, OKX, Bybit, Bitget, Coinbase, Nexo, or wherever, (no judgement, really) the easiest move is to use their savings or earn products.

Right now, depending on the platform and whether you lock it up or keep it flexible, you're looking at roughly 2% to 8% APY for flexible savings, with fixed terms going higher and some loyalty programs advertising more if you jump through enough hoops (holding their native token, locking for months, etc).

But I want to be very clear about what is actually happening here.

This yield is not Circle or Tether sharing their profits with you still. It is the exchange running a campaign, paying you out of their own pocket, so you keep your money on their platform and they can lend it out, use it for liquidity, or borrow it for their own operations. You are essentially loaning your stables to the exchange.

Option 2: Actually own a stablecoin that shares the yield with you

This is where it gets interesting, VERY interesting.

Some newer stablecoins are built so that the yield generated by the underlying assets flows back to the holder, not to the issuer. You stop being the product and start being the participant.

But before we go through them, there's something important to understand because it will change how you think about each option. There are two different ways these stablecoins deliver yield to you, and the user experience is very different depending on which model you're using.

WTF YOU MEAN JANA??? MODEL??

Relax, model here is just the route these coins will pay you interest, giving you in return for you trusting them and using their token.

Inside Option 2: There are two models

Model 1: You have to stake to earn

You hold the base stablecoin (DAI, USDS, USDe), and on its own it does nothing. It just sits at $1.

To earn yield, you have to actively deposit it into a separate staked version (sDAI, sUSDS, sUSDe) through another transaction.

Now you hold a different token, and that one grows over time.

If you want to spend or send your stables, you often have to unstake first, which means another transaction and more gas.

The yield exists, but it's gated behind actions you have to remember to take.

Model 2: The token grows on its own

You hold the token, and it grows in your wallet automatically.

No staking, no second token, no extra steps.

This is how USDY works. You just buy it and hold it.

The downside is that the token's price is not pinned at $1, so it's harder to use as a unit of account in DeFi or payments.

Stablecoins Options Worth Knowing

DAI and sDAI (MakerDAO, now Sky)

DAI is the original decentralised stablecoin.

It's not issued by a company holding your dollars in a bank. It's minted by smart contracts when users lock up collateral (ETH, other crypto, and increasingly tokenised real-world assets like US Treasuries) at over-collateralised ratios. If your collateral drops in value, the protocol liquidates it automatically to keep DAI backed.

DAI on its own sits at $1 and doesn't pay you anything, just like USDC. To earn, you stake it into sDAI and start collecting the DAI Savings Rate, which comes from real protocol revenue including the yield on the Treasuries in their reserve. The yield is structural. It belongs to the holder by design, not to a company keeping it for themselves.

DAI's market cap sits around $5 billion, and its newer sibling USDS (the rebranded version under Sky) is above $7.5 billion, so together the ecosystem is bigger than most people think. Still much smaller than USDC and USDT, but the model is fundamentally different. No central issuer can freeze your balance. The system runs on code and collateral.

The trade-off:

You have to interact with smart contracts more often. Staking, unstaking, moving between DAI and sDAI, all on-chain transactions.

Each interaction costs gas and exposes you to smart contract risk, even if the contracts are battle-tested.

If you want to spend, send, or trade your DAI, you usually have to unstake from sDAI first.

USDe and sUSDe (Ethena)

Synthetic dollar, around $4.4 billion market cap today.

And here is the most important update: when I wrote the first version of this article in April, USDe was at $5.8 billion. That is not a red flag, but it tells you something about this model, it breathes with market conditions instead of just growing in a straight line.

It maintains its peg through a delta-hedging strategy using staked ETH and short positions on perpetuals. Its yield comes from funding rates and staking rewards, not from a company holding Treasuries.

Same staking model as DAI, you hold USDe to keep it at $1, you stake into sUSDe to collect the yield.

The trade-off is that USDe is not backed by dollars in a bank, so understanding how the hedge works matters before you trust it with size. When perpetual funding rates go negative for extended periods, the yield model is under more stress.

USDY (Ondo)

This one is even more interesting in my opinion.

USDY is a tokenised yield-bearing note backed by short-term US Treasuries and bank deposits. It sits around $2 billion in market cap now.

It is not pinned at $1. Instead, the token's value slowly increases over time as it accrues yield. It's basically a tokenised T-bill.

This is the Model 2 I mentioned. You don't have to stake anything. You buy USDY, you hold it, and it grows in your wallet on its own.

No second token, no extra transactions, no toggling between staked and unstaked versions every time you want to move funds.

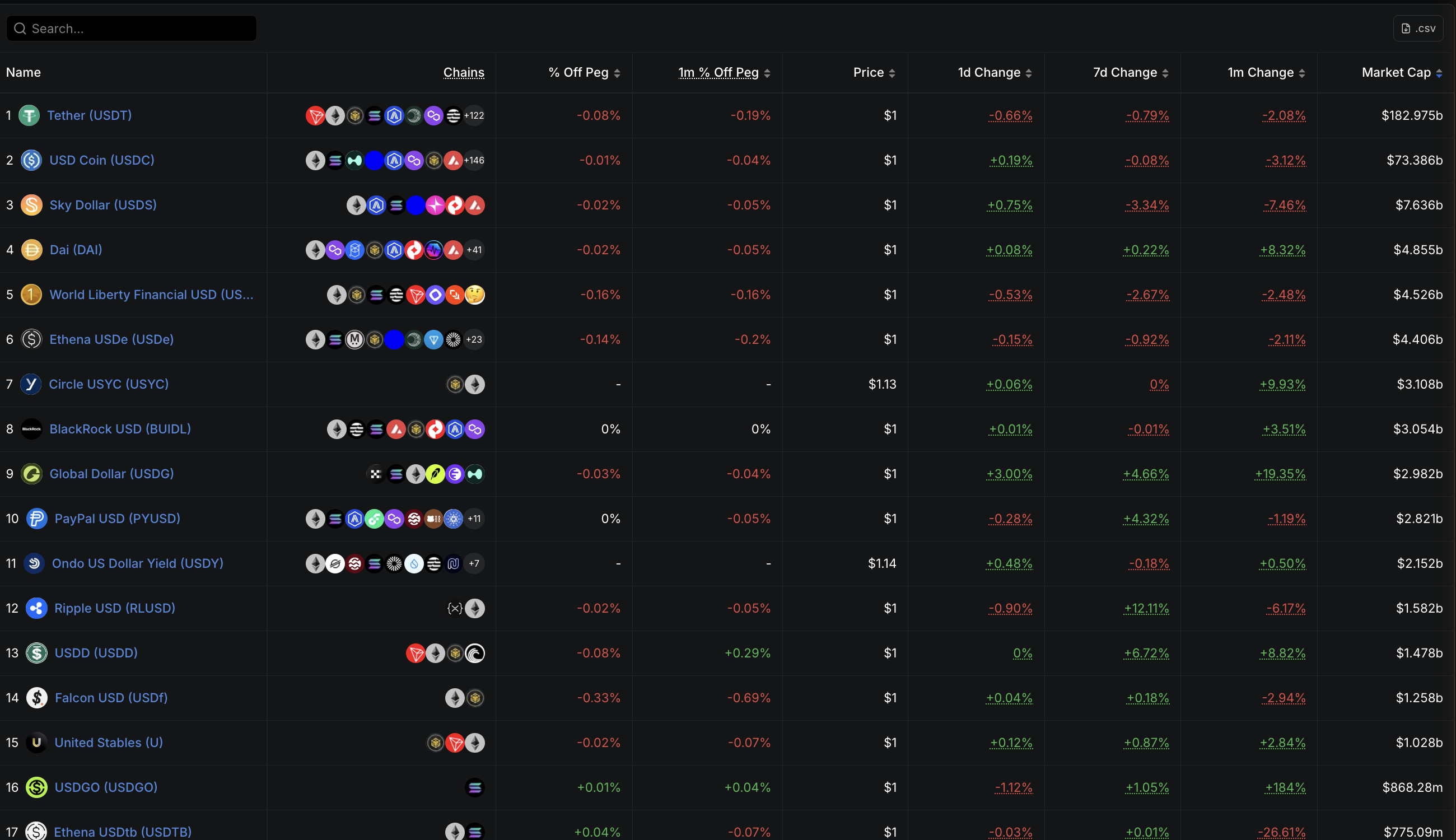

You can even see it on the live ranking table. Every stablecoin sitting at $1, and USDY sitting at $1.14. That difference is the yield, accrued right inside the token.

Source: DefiLlama, top stablecoins by market cap, July 8 2026

Besides the research I did on this one last time I also tested

After the first version of this article, I decided to run the test myself.

I put 1k into USDY and let it sit for a month.

No staking.

No touching.

Just holding.

Here is what my 1k did:

On rare occasions I saw it dip to 997.

The rest of the time it held steady, and it settled at 1005.

My money grew while sitting still, in my own wallet, with nothing for me to do. For anyone looking to keep their money in a stable paired with something extra, this is a type of edge the other options don't offer, in my opinion.

The KYC part, because it is the price of entry

USDY requires KYC, and not a light one. I had to answer a lot of questions, more than I expected. It is not available to US persons and some other jurisdictions, and Ondo is a centralised issuer holding the Treasuries. So you're trading some decentralisation for a much cleaner experience. It's TradFi wrapped in a token, but the wrapper is properly done.

And here is my real experience with the process: I am not a US citizen, I submitted my application, and I got my approval in less than 24 hours. Pretty seamless.

Source: my own Ondo onboarding emails

Why this option, really (a parenthesis on trust)

Let me open a parenthesis here, because this is the real reason I went for this option and not one of the staking models.

I am living a phase where I don't trust any contract enough to keep my wallet connected for a soft or a hard stake.

For the ones new here, let's just break this for a second:

A soft stake is flexible. You deposit your tokens into a contract and can pull them out anytime.

A hard stake locks them. Your tokens sit in the contract for a fixed period and you wait to get them back.

Either way, your money leaves your wallet and lives inside someone else's smart contract. And every contract you stay connected to is one more door that can be opened by someone that isn't you. We have all seen enough drained wallets to know the door doesn't need to be left open for long.

Maybe this phase of mine will pass, maybe it won't. But right now, a token that grows on its own, inside my own wallet, with nothing to sign and nothing to connect after the buy, fits exactly where my head is.

Closing the parenthesis.

The new names growing fast (and what they don't share)

Since April, some names most people hadn't heard of a year ago took real space. Let's look at the fastest growing ones:

USD1 (World Liberty Financial), around $4.5 billion already, the fifth largest stablecoin.

PYUSD (PayPal), close to $3 billion, and since it expanded to Solana the fees dropped from dollars to fractions of a cent.

RLUSD (Ripple), around $1.6 billion and climbing.

Big names, growing fast.

Now the question this whole article taught you to ask: which of them shares the yield with you, the holder?

None of them.

All three run the same model as USDT and USDC. Your dollars go into Treasuries, the issuer collects the yield, your token sits at $1 forever.

So the fastest growing stablecoins of 2026 are still built on you getting nothing, which in my opinion proves the point of this article more than anything I could write.

What Jana is Doing

Since you asked last time, here's the honest breakdown of where I personally sit right now.

This is not a recommendation. It's just where I've landed after thinking through everything in this article, and my situation is not your situation.

I moved my stablecoin holdings from USDT to USDC.

Not because USDC is perfect, but because at least it's making more of an effort on the things that matter to me: more transparent reserves, more regulatory clarity, and a slightly less aggressive posture about keeping every dollar of yield to itself. Both companies still pocket the Treasury yield, I'm not pretending otherwise, but between the two giants, USDC is the one I'm willing to hold for now.

And the smaller portion I said I would put into USDY in April is no longer a plan. It's done, tested for a month, and staying. You read what my 1k did.

I want to be clear about the bigger picture too.

I'm a heavily conservative BTC lover first.

Stablecoins, for me, are not the main game. They're the operational layer and a small diversification piece, not where I'm trying to build long-term wealth.

BTC is where I anchor.

Stablecoins are where I move, transact, and park dollars I might need to deploy.

A note before we close

This is not financial advice and should not be read as such. Read this article, then go do your own research and form your own conclusions. I don't know you, I don't know your situation, and you shouldn't trust any of my claims without verifying them yourself.

Nothing in this piece is an endorsement of any specific platform, protocol, or token. It's an honest look at where the stablecoin space is right now, written for people trying to think about it more carefully. The decisions are yours.

That's always been the deal in Web3.

You get sovereignty, but the work of being your own bank means actually doing the work.

Read, question, verify, decide. Then act.

OFC DON'T FORGET TO SHARE!!

References

The first version of this article, April 28 2026: x.com/JanaCryptoQueen/status/2049020517903139201

DefiLlama stablecoins dashboard, where all market data in this article comes from, as of July 8 2026: defillama.com/stablecoins

Ondo Finance, USDY official page: ondo.finance/usdy

Ethena, USDe: ethena.fi

Sky (former MakerDAO), DAI and USDS: sky.money